卧的贸易孝 1951 Chapter 6 Managing Liabilities

Chapter 6 Chapter 6 Managing Liabilities Managing Liabilities

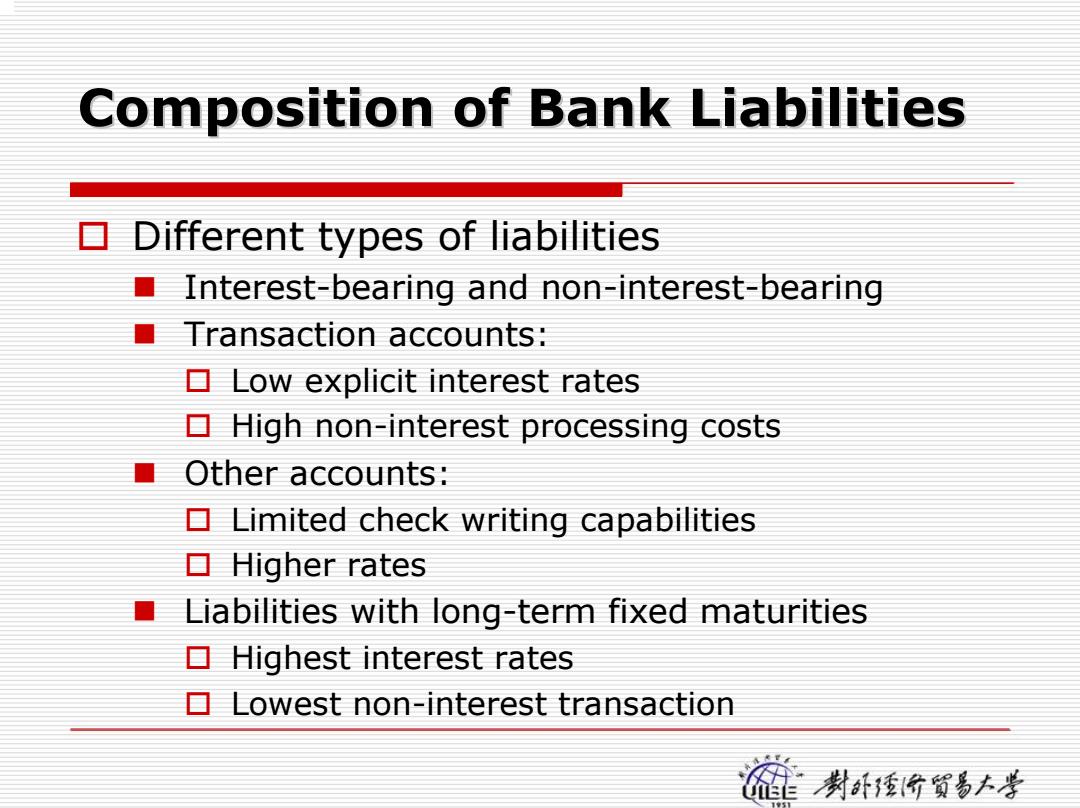

Composition of Bank Liabilities Different types of liabilities Interest-bearing and non-interest-bearing ■ Transaction accounts: Low explicit interest rates High non-interest processing costs ■ Other accounts: Limited check writing capabilities ▣Higher rates Liabilities with long-term fixed maturities Highest interest rates Lowest non-interest transaction 爸封强的黄香+孝

Composition of Bank Liabilities Composition of Bank Liabilities Different types of liabilities Interest-bearing and non-interest-bearing Transaction accounts: Low explicit interest rates High non-interest processing costs Other ac c ounts: Limited check writing capabilities Higher rates Liabilities with long-term fixed maturities Highest interest rates Lowest non-interest transaction

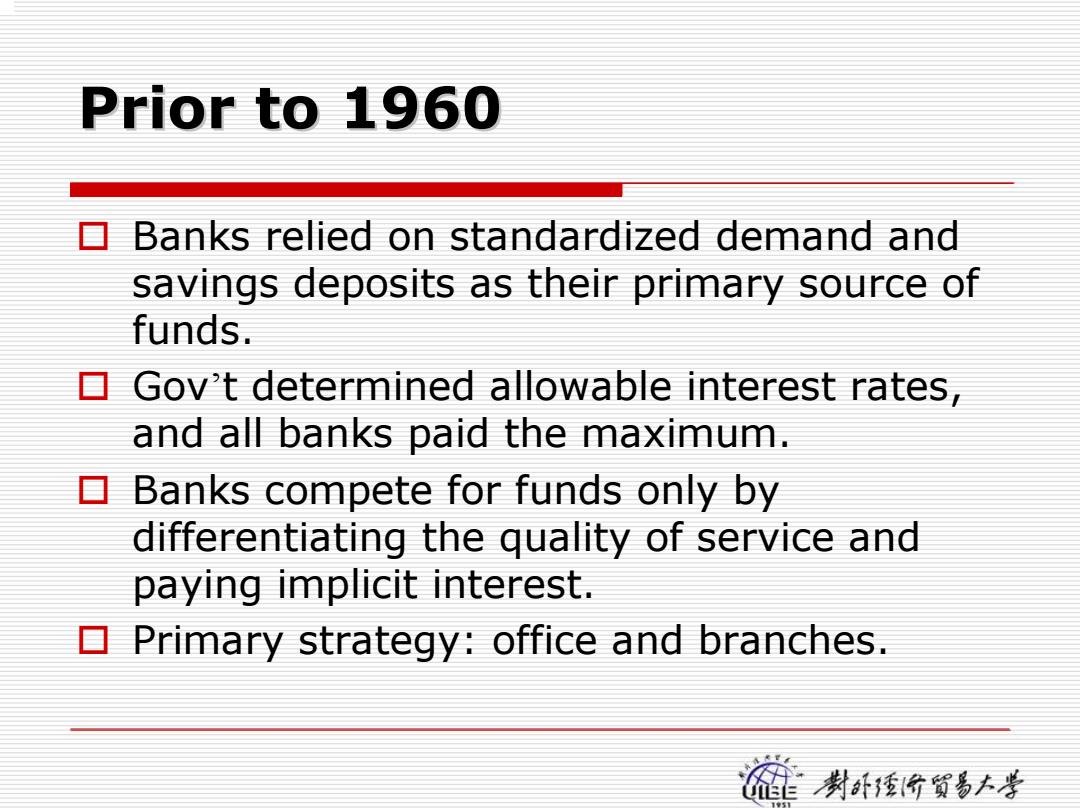

Prior to 1960 Banks relied on standardized demand and savings deposits as their primary source of funds. Gov't determined allowable interest rates, and all banks paid the maximum. 目 Banks compete for funds only by differentiating the quality of service and paying implicit interest. Primary strategy:office and branches. 麓的贫香小手

Prior to 1960 Prior to 1960 Banks relied on standardized demand and savings deposits as their primary source of funds. Gov’t determined allowable interest rates, and all banks paid the maximum. Banks compete for funds only by differentiating the quality of service and paying implicit interest. Primary strategy: office and branches

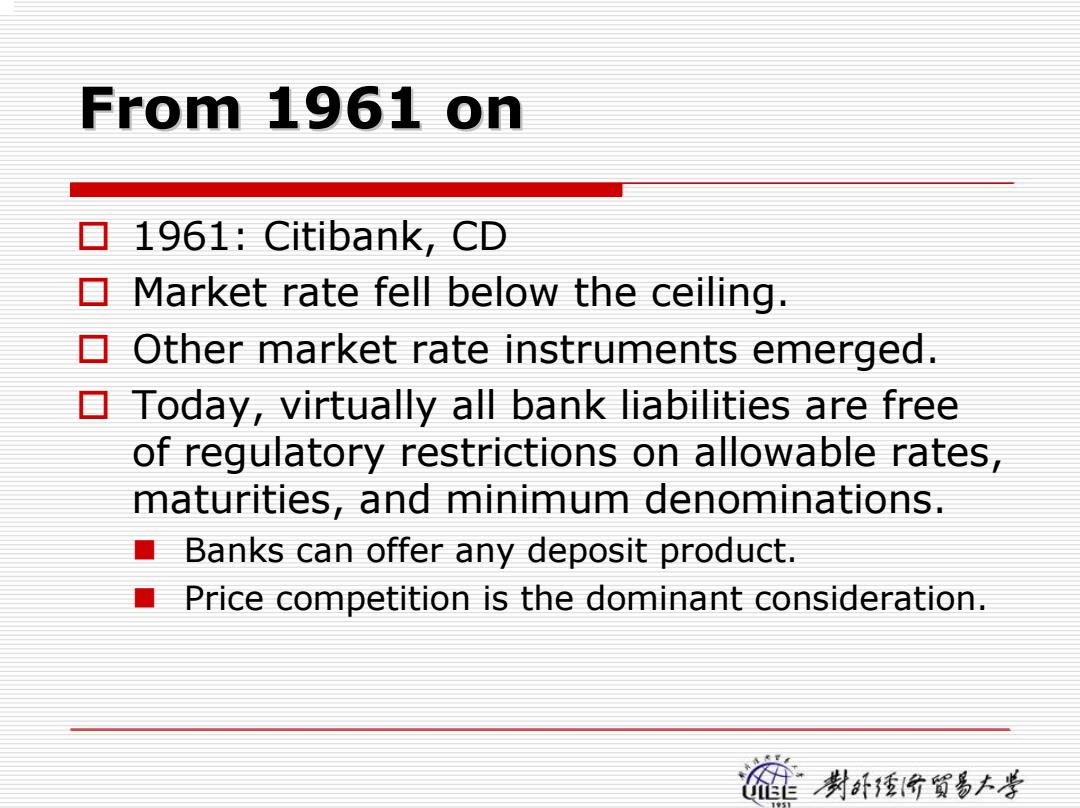

From 1961 on ▣1961:Citibank,CD Market rate fell below the ceiling. Other market rate instruments emerged. Today,virtually all bank liabilities are free of regulatory restrictions on allowable rates, maturities,and minimum denominations. ■ Banks can offer any deposit product. ■ Price competition is the dominant consideration. 爸封强的黄香+孝

From 1961 on From 1961 on 1961: Citibank, CD Market rate fell below the ceiling. Other market rate instruments emerged. Today, virtually all bank liabilities are free of regulatory restrictions on allowable rates, maturities, and minimum denominations. Banks can offer any deposit product. Price competition is the dominant consideration

Problems created by the freedom Customers have become much more rate conscious:interest elastic. Customers prefer shorter-term deposits strongly:lower interest rate risk. Liabilities become more rate sensitive Pricing assets becomes more difficult 猫1竹對+手

Problems created by the Problems created by the freedom freedom Customers have become much more rate conscious: interest elastic. Customers prefer shorter-term deposits strongly: lower interest rate risk. Liabilities become more rate sensitive Pricing assets becomes more difficult