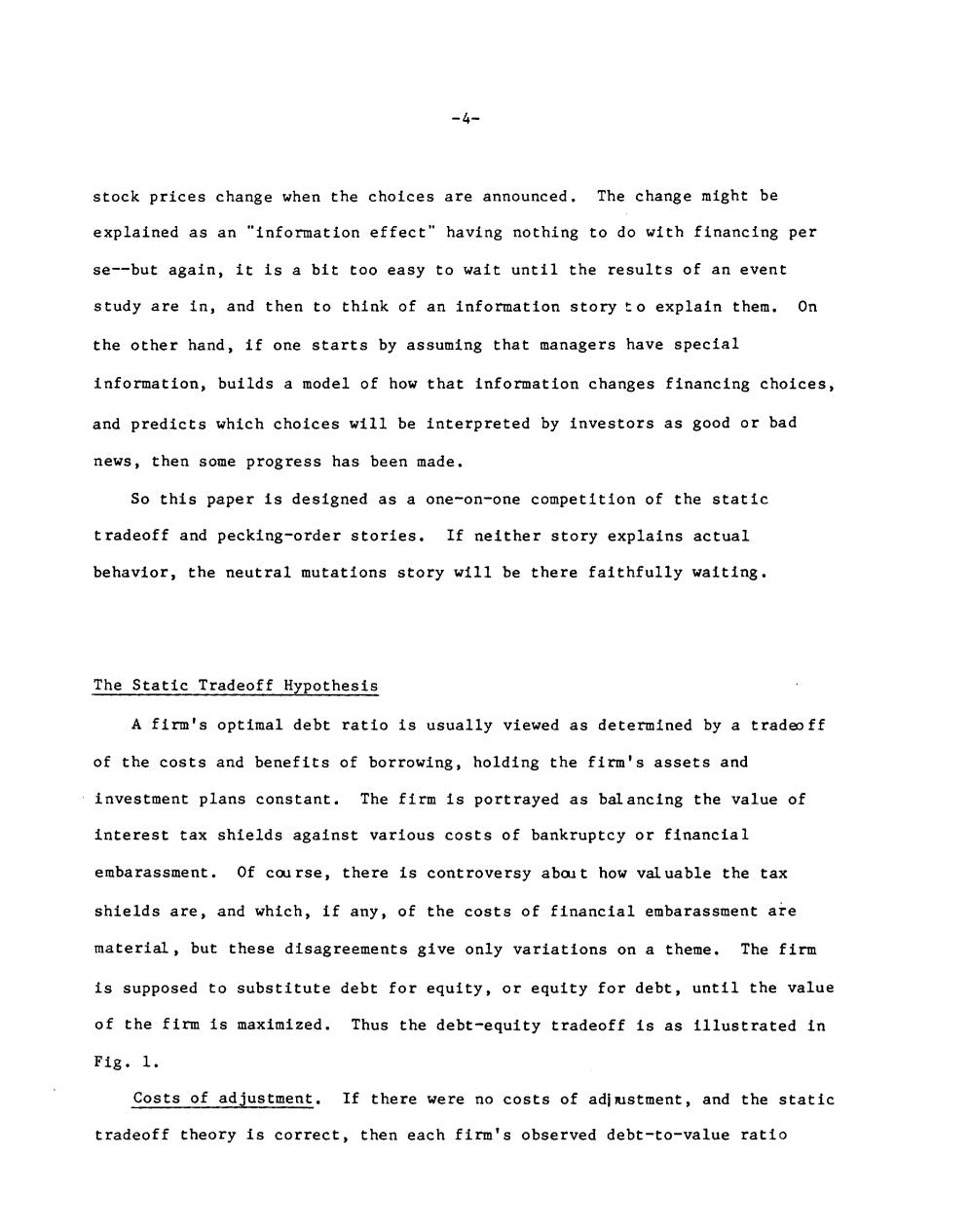

-4- stock prices change when the choices are announced.The change might be explained as an "information effect"having nothing to do with financing per se--but again,it is a bit too easy to wait until the results of an event study are in,and then to think of an information story to explain them.On the other hand,if one starts by assuming that managers have special information,builds a model of how that information changes financing choices, and predicts which choices will be interpreted by investors as good or bad news,then some progress has been made. So this paper is designed as a one-on-one competition of the static tradeoff and pecking-order stories.If neither story explains actual behavior,the neutral mutations story will be there faithfully waiting. The Static Tradeoff Hypothesis A firm's optimal debt ratio is usually viewed as determined by a tradeo ff of the costs and benefits of borrowing,holding the firm's assets and investment plans constant.The firm is portrayed as bal ancing the value of interest tax shields against various costs of bankruptcy or financial embarassment.Of course,there is controversy about how val uable the tax shields are,and which,if any,of the costs of financial embarassment are material,but these disagreements give only variations on a theme.The firm is supposed to substitute debt for equity,or equity for debt,until the value of the firm is maximized.Thus the debt-equity tradeoff is as illustrated in F1g,1. Costs of adjustment.If there were no costs of adjustment,and the static tradeoff theory is correct,then each firm's observed debt-to-value ratio

-5- should be its optimal ratio.However,there must be costs,and therefore lags,in adjusting to the optimum.Firms can not immediately offset the random events that bump them away from the optimum,so there should be some cross-sectional dispersion of actual debt ratios across a sample of firms having the same target ratio. Large adjustment costs could possibly explain the o bserved wide variation in actual debt ratios,since firms would be forced into long excursions away from their optimal ratios.But there is nothing in the usu 1 static tradeoff stories suggesting that adjustment costs are a first-order concern--in fact, they are rarely mentioned.Invoking them withoit modelling them is a cop-out. Any cross-sectional test of financing behavior should specify whether 。 firms'debt ratios differ because they have different optimal ratios or because their actual ratios diverge from optimal ones.It is easy to get the two cases mixed up.For example,think of the early cross-sectional studies which attempted to test MM's Proposition I.These studies tried to find out whether differences in leverage affected the market value of the firm (or the market capitalization rate for its operating income).With hindsight,we can quickly see the problem:if adj ustment costs are small,and each firm in the sample is at,or close to its optimum,then the in-sample dispersion of debt ratios must reflect differences in risk or in other variables affecting optimal capital structure.But then MM's Proposition I cannot be tested unless the effects of risk and other variables on firm value can be adjusted for.By now we have learned from experience how hard it is to hold "other things constant"in cross-sectional regressions. Of course,one way to make sense of these tests is to assume that adjnustment costs are small,but managers don't know,or don't care,what the

-6- optimal debt ratio is,and thus do not stay close to it.The researcher then assumes some (usually unspecified)"managerial"theory of capital structure choice.This may be a convenient assumption for a cross-sectional test of MM's Proposition I,but not very helpful if the object is to understand financing behavior,3 But suppose we don't take this "managerial"fork.Then if adjustment costs are small,and firms stay near their target debt ratios,I find it hard to understand the o bserved diversity of capital structures across firms that seem similar in a static tradeoff framework.If adjustment costs are large, so that some firms take extended excursions away from their targets,then we ought to give less attention to refining our static tradeoff stories and relatively more to understanding what the adjuustment costs are,why t hey are so important,and how rational managers would respond to them. But I am getting ahead of my story.On to debt and taxes. Debt and taxes.Miller's famous "Debt and Taxes"paper [26]cut us loose from the extreme implications of the original MM theory,which made interest tax shields so valuable that we could not explain why all firms were not awash in debt.Miller described an equilibrium of aggregate supply and demand for coporate debt,in which personal income taxes paid by the marginal investor in corporate debt just offset the corporate tax saving.However,since the equilibrium only determines aggregates,debt policy should not matter for any single tax-paying firm.Thus Miller's model allows us to explain the dispersion of actual debt policies without having to introduce non-value-maximizing managers,4 Trouble is,this explanation works only if we assume that all firms face approximately the same marginal tax rate,and that is an assumption we can

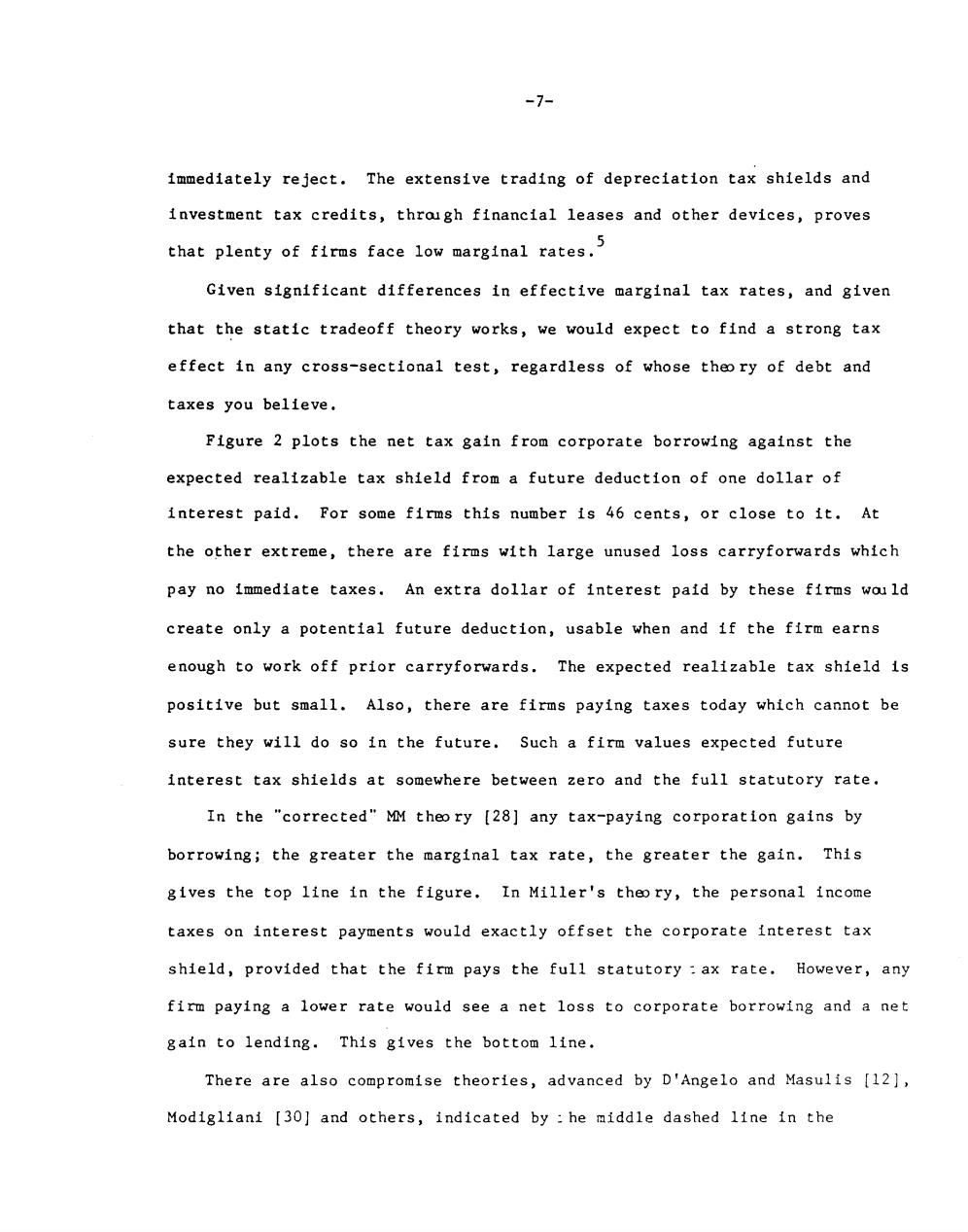

-7- immediately reject.The extensive trading of depreciation tax shields and investment tax credits,throigh financial leases and other devices,proves 5 that plenty of firms face low marginal rates. Given significant differences in effective marginal tax rates,and given that the static tradeoff theory works,we would expect to find a strong tax effect in any cross-sectional test,regardless of whose theo ry of debt and taxes you believe, Figure 2 plots the net tax gain from corporate borrowing against the expected realizable tax shield from a future deduction of one dollar of interest paid.For some firms this number is 46 cents,or close to it.At the other extreme,there are firms with large unused loss carryforwards which pay no immediate taxes.An extra dollar of interest paid by these firms would create only a potential future deduction,usable when and if the firm earns enough to work off prior carryforwards.The expected realizable tax shield is positive but small.Also,there are firms paying taxes today which cannot be sure they will do so in the future.Such a firm values expected future interest tax shields at somewhere between zero and the full statutory rate. In the "corrected"MM theo ry [28]any tax-paying corporation gains by borrowing;the greater the marginal tax rate,the greater the gain.This gives the top line in the figure.In Miller's theo ry,the personal income taxes on interest payments would exactly offset the corporate interest tax shield,provided that the firm pays the full statutory ax rate.However,any firm paying a lower rate would see a net loss to corporate borrowing and a net gain to lending.This gives the bottom line. There are also compromise theories,advanced by D'Angelo and Masulis [12], Modigliani [30]and others,indicated by he middle dashed line in the

-8- figure.The compromise theories are appealing because they seem less extreme than either the MM or Miller theories.But regardless of which theory holds,the slope of the line is always positive.The difference between (1) the tax advantage of borrowing to firms facing the full statutory rate,and (2)the tax advantage of lending (or at least not borrowing)to firms with large tax loss carryforwards,is exactly the same as in the "extreme" theories.Thus,although the theories tell different stories aboit aggregate supply and demand of corporate debt,they make essentially the same predictions aboit which firms borrow more or less than average. So the tax side of the static tradeoff theory predicts that IBM should borrow more than Bethlehem Steel,other things equa1,and that General Motors' debt-to-value ratio should be more than Chrysler's. Costs of financial distress.Costs of financial distress include the legal and administrative costs of bankruptcy,as well as the subtler agency, moral hazard,monitoring and contracting costs which can erode firm value even if formal default is avoided.We know these costs exist,although we may debate their magnitude.For example,there is no satisfactory explanation of debt covenants unless agency costs and moral hazard problems are recognized. The literature on costs of financial distress supports two qualitative statements about financing behavior.6 1.Risky firms ought to borrow less,other things equa l.Here "risk"would be defined as the variance rate of the market value of the firm's assets.The higher the variance rate,the greater the probability of default on any given package of debt claims.Since costs of financial distress are caused by threatened or actul default,safe firms oght to